Forecast for financial markets: cloudy skies, then potential sun

With midterms approaching, near-term uncertainty is rising but a more stable stretch could follow

Lectura de 5 minutos

PUNTOS CLAVE

- Election outcomes often influence which sectors outperform, but long-term market performance tends to depend more on earnings growth and economic fundamentals than politics alone.

- Strong stock market performance is no longer primarily coming from just a handful of big technology companies.

- AI remains a powerful investment theme, but investors are increasingly rewarding companies that can translate AI spending into earnings and long-term returns.

As financial markets look ahead to the midterm elections, the pattern looks familiar but with a different hue.

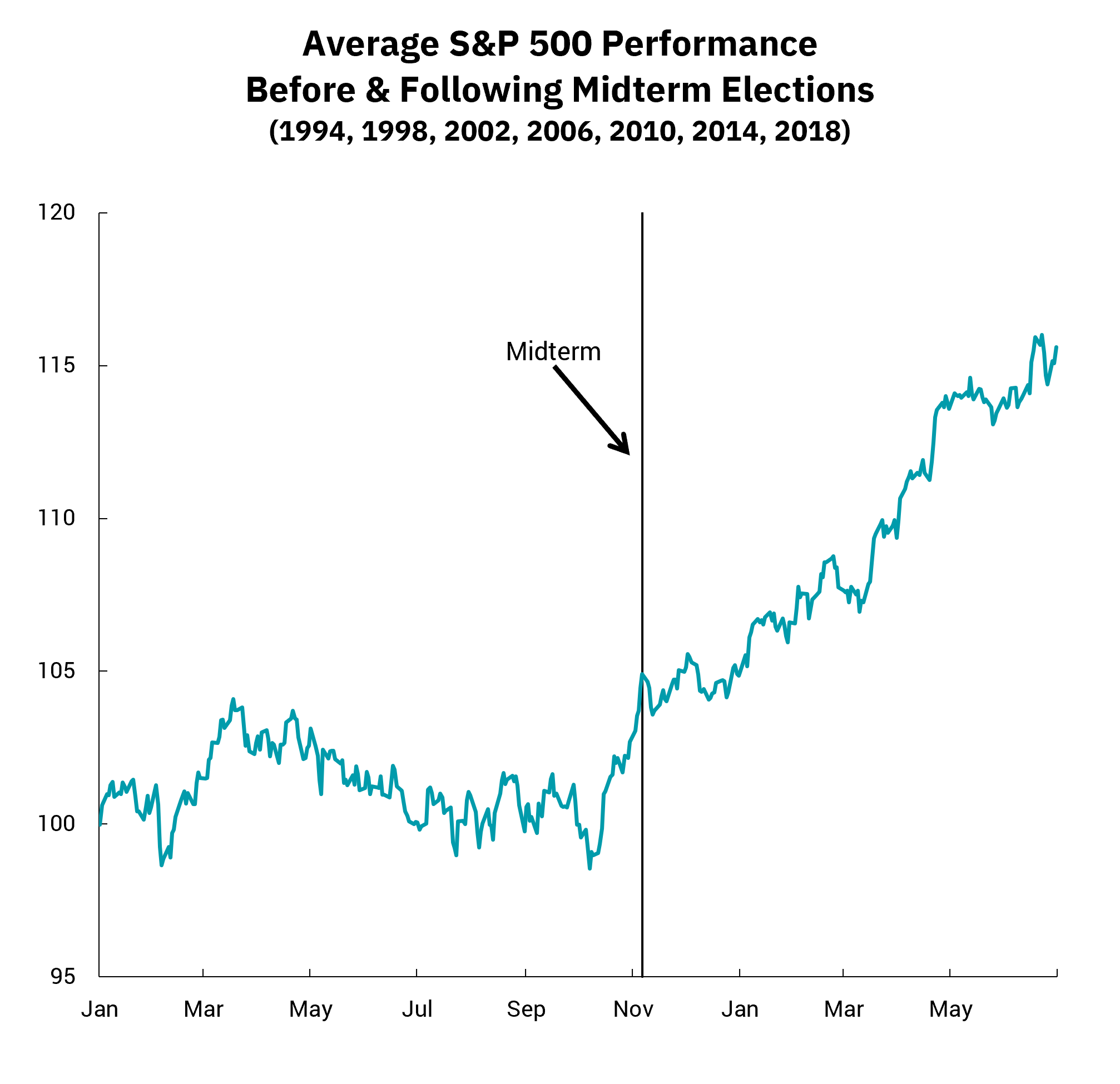

“There’s usually more uncertainty leading up to midterms,” said Brian Henderson, director de inversiones en BOK Financial®. This uncertainty comes from investors trying to weigh different policy outcomes and what they could mean for markets. However, that sentiment doesn't tend to last, according to Henderson. "After the midterms, markets almost always do well," he said.

Fuente: Strategas

As Strategas data shows, performance leading up to the midterms is uneven and volatile, but once the election passes, the trend turns more decisively higher, with gains becoming more consistent over time.

However, that's not to say that different election results don't have varying effects on markets. These effects tend to play out in sector performance.

"If you think about different outcomes, you tend to see different areas respond," Henderson said. "For example, more defense spending tends to benefit aerospace and defense names, while energy can look very different depending on how supportive the policy environment is for production."

Healthcare is another area that can move quickly, he added. "You can see the healthcare sector react depending on how much focus there is on pricing or regulation," Henderson explained, noting that even modest policy shifts can change how healthcare-related stocks are traded.

Yet even with those differences, the broader pattern tends to hold. "It's usually more about which sectors lead than whether the market itself does well," Henderson said.

And so, for financial markets, midterms may be the backdrop, while ongoing trends may be at center stage.

Stock performance is broadening

For instance, equities are no longer being carried by a single group of companies. Earnings estimates for 2026 remain strong and are broadening beyond the largest technology companies. This could mean that even "average" stocks in the S&P 500, as well as mid- and small-cap companies, could post positive relative performance.

“It’s been a pretty narrow market, and the next step is seeing that broaden out,” said Steve Wyett, director de estrategias de inversión de BOK Financial.

Some of that rotation is cyclical. Some of it is structural. Finally, some of it, as Henderson pointed out, reflects the uncertainty around the election cycle-shifts in spending priorities, regulation and policy direction that can tilt the playing field across sectors.

At the same time, earnings expectations are rising across the board, which may mean that performance starts to diverge. That's because, as earnings expectations move higher, it becomes more difficult for companies to meet them, which tends to widen the gap between companies that deliver and those that fall short. "As expectations rise, you're going to see a much wider range of outcomes across companies," said Matt Stephani, presidente de Cavanal Hill Investment Management, Inc., una subsidiaria de BOK Financial Corporation.

AI is still the driver but no longer enough on its own

Meanwhile, artificial intelligence (AI) remains the central force behind much of the market's momentum. "This is one of the largest capital-expenditure cycles we've seen," Wyett said, pointing to the scale of investment still flowing through infrastructure, data centers and related technologies.

However, the way that theme shows up in markets is changing. "The question now is who turns that investment into actual returns," Stephani said, and that's where the next phase of the market likely will be decided.

Earlier, broad exposure to AI was often rewarded. Now, results matter. Companies that can translate spending into earnings are starting to separate themselves from those that cannot. In that sense, AI is reinforcing a broader shift already underway-toward a market defined more by dispersion than by a single rising tide, a dynamic Stephani sees playing out across sectors.

What’s ahead for bonds and the credit market

While equities are rotating, fixed income has already repriced. As Henderson said, "The bond market has had to reprice pretty quickly-and that's created both risk and opportunity."

The most immediate effect is straightforward: bonds are generating income again. In Wyett's words: "For the first time in a long time, fixed income can actually contribute meaningfully to returns."

Meanwhile, at a high level, credit markets are "holding up well," Henderson said. Credit spreads have widened but not to levels signaling trouble, and corporate fundamentals continue to support the market. However, that stability is not uniform-and it may not hold as cleanly if conditions tighten.

There's been a lot of growth in credit markets, especially on the private side," Henderson said, noting that capital has flowed quickly into areas that historically were more limited and less visible. "That doesn't always come with the same level of liquidity or transparency."

That matters more in a market where conditions are evolving. As a result, some areas of credit, such as less liquid areas where it's harder to exit, are more vulnerable than others. As Stephani said, "You're starting to see more differentiation across credit."

And so, instead of a single stress point, the risk is more fragmented. "It's not that credit looks broken," Henderson said. "It's that some areas are going to matter more than others."

Read more of our Actualización del mercado a mitad del año 2026.